The implications of Crude Oil Inventory build-up & recent price increase

Is this demand erosion?

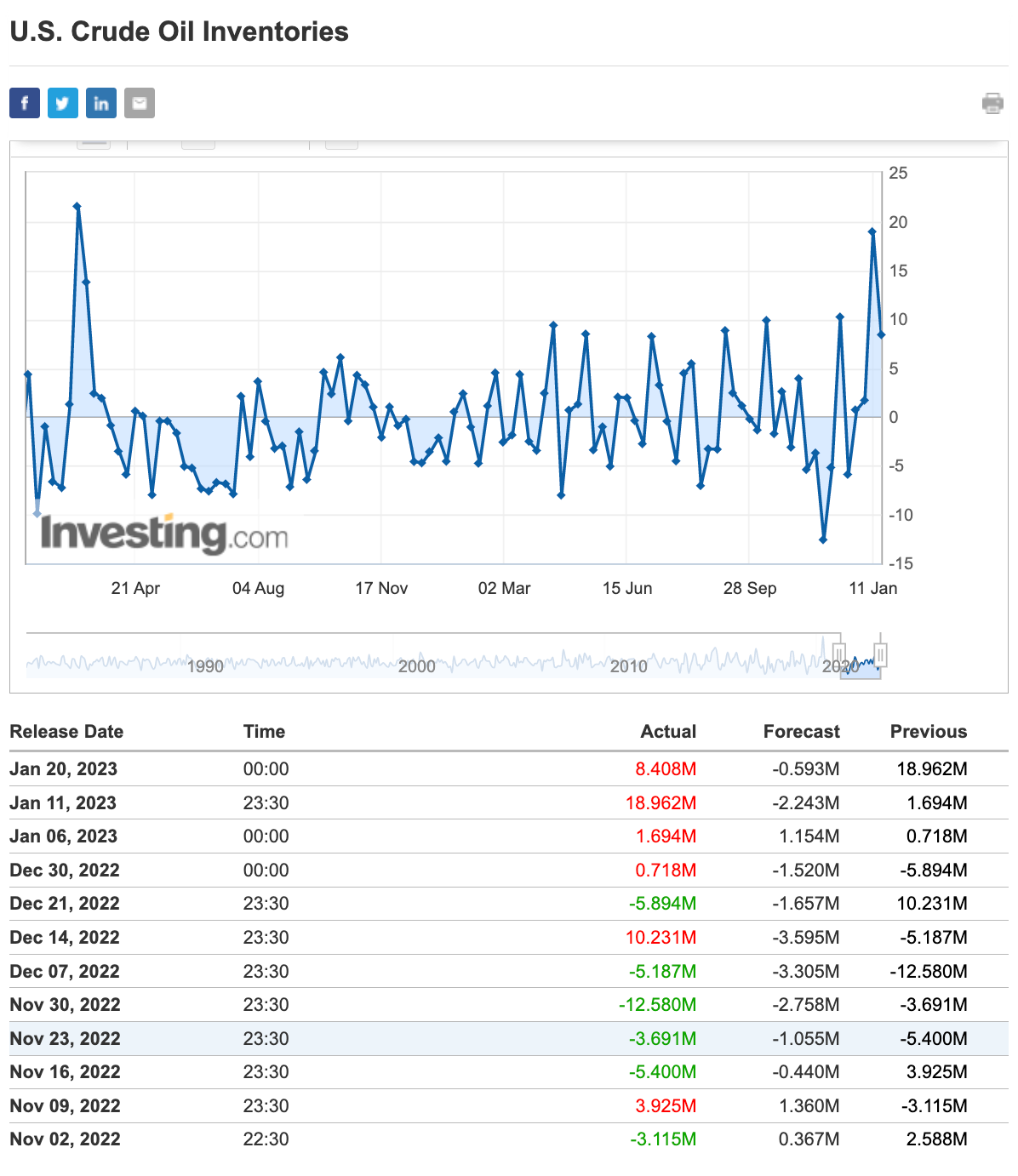

The latest US Crude Oil Inventories figure was released as of 19 Jan 2023 (EST). The market has a forecast of -0.593M but the actual inventory came up to 8.408M.

Souce: https://www.investing.com/economic-calendar/eia-crude-oil-inventories-75

As per the screenshot, the increase in inventory has the following implication:

If the increase in crude inventories is more than expected, it implies weaker demand and is bearish for crude prices.

Since Jan 2023, the crude oil inventory has been increasing, higher than expected. This means that the producers are not “consuming” crude oil as much.

The implications of the current trend

Crude Oil inventory can be seen as a guide for market consumption (and thus demand). Taking a look around us, there are oil-related products surrounding us. From the make-up that we use, the plastics around us, the roads that are laid (using bitumen, a product from oil), the lubricants that are essential for machines and the energy that we consume, oil has a strong & undeniable presence in our lives & our economies.

With price being the result of demand and supply, factors of both demand and supply will lead to the movements of the stock price. Oil is a universal product with some analysts crediting the oil price increase to China opening up after 3 years of Covid restrictions. This can mask the demand erosion in other countries, including the US which has been hit by stubborn inflation. Such inflationary pressures have led to reduced disposable income for many.

To the trend of increasing crude oil inventory in the US, my “interpretation” is that the producers are anticipating lesser consumption arising from lesser demand. This implies that there will be lesser oil-related products hitting the markets in the coming weeks. Thus, we should not be “buoyed” by the recent WTI oil price increase. We need to look into the factors leading to the price increase with consideration incorporating both demand & supply components. This could be the case of China's rising demand exceeding the US's decline in consumption.

With China establishing a strategic relationship with OPEC+ and working on non-USD deals, there seem to be more headwinds coming for the US. From PetrolYuan (partial payment for oil purchase in China’s RMB currency) and a 30-year LNG contract with Qatar, China is establishing economic partnerships that consolidate its position as a global power. Let us continue to monitor the coming earnings season closely. Let us pay attention to the market outlook, beyond the typical revenue and EPS. These data will help us to understand the extent of demand erosion affecting the USA.

Such macro considerations can help us to better navigate the volatile market. While many have expressed relief in the recent rallies, the coming days will confirm if it is a dead cat’s bounce or the reversal that many hope for. Personally, I am hopeful for the best but prepared for the worst. Given the metrics, I remain bullish for a bearish outlook. Let us do our due diligence - research before we invest.